PhilHealth contribution for OFWs: how much to pay, how to pay and check status

Learn the PhilHealth contribution for OFWs, including current rates, payment options, how to pay from abroad and how to check your status.

💳 Get your free digital card

Managing your money abroad as an OFW can be complex, particularly if you’re handling foreign currencies, sending money home, and saving for your future.

For this reason, there are various options for an OFW savings account available to support day-to-day transactions and long-term financial goals.

This guide covers popular options like the BPI OFW savings account, Metrobank OFW savings account, and PNB OFW savings account, including the requirements and opening process you can expect. We'll also introduce the Wise account, a handy companion to make your money go further with low, transparent fees.

| Table of Contents |

|---|

Sign up for a free account now

An OFW savings account is a bank account designed to meet the needs of Filipinos working abroad who are saving or sending remittances home.

Depending on the product, you can usually hold a balance, receive and send payments digitally, and manage your money through an app or online banking.

Some accounts also come with minimum opening or maintaining balance requirements, which you’ll need to meet to avoid fees or earn interest.

Here are a few things to consider when selecting the right OFW savings account for your needs:

There are several OFW savings account options available from major banks in the Philippines.

These products differ in how they handle maintaining balances, remittance fees, and account access. Some are designed mainly for sending and receiving money, while others are better suited for saving and earning interest.

Here are some commonly used options.

There are several BPI OFW savings account options available under the BPI Pinoy Abroad program¹, allowing you to choose based on your needs.

Key features:

For example, the Pamana Padala account² is designed for remittances, with a minimum initial deposit of PHP 500 and no maintaining balance required.

However, there may be inward remittance costs if you're receiving payments from overseas, typically around PHP 150 for peso accounts³.

If your focus is saving, the Pamana Savings account⁴ may be more suitable, particularly if you can maintain a balance of at least PHP 25,000 to earn interest.

The process of how to open a BPI savings account depends on the product, but you’ll usually need to visit a branch with your ID.

The Metrobank OFW savings account has no minimum deposit requirement, but you’ll need to maintain at least PHP 10,000 to earn interest⁵.

Key features:

The account is designed to give easy access to funds, with a linked debit card for day-to-day spending.

You can manage your money on the move using the Metrobank app and Metrobank Online, and send remittances home whenever needed.

Metrobank also has partnerships with banks globally, allowing in-person remittances from countries including the US, Singapore, China, Japan, and Korea. This can be helpful if you prefer branch-based services while abroad.

There are several options for a PNB OFW savings account, which you can open in the Philippines before you travel, through the PNB app, or via the PNB Global Filipino hub⁶.

Key features:

The Global Filipino hub has representatives in various countries, including Hong Kong and Singapore, as well as major destinations like the US.

Account features depend on the specific product you choose, but PNB focuses on offering accessible remittance services and support for Filipinos overseas.

You can open a BDO Kabayan savings account⁷ to hold either PHP or US dollars, with a fully remote digital application process.

Key features:

To open the account, requirements include submitting a valid ID, complete a video call for verification, and depositing your chosen amount online.

However, although you can open the account remotely, you may not be able to receive your passbook or debit card until you return to the Philippines.

You can open an OFW savings account in person or, in many cases, online. Individual banks set their own processes for account opening, including the eligibility requirements and the ID documents you’ll need to provide. Let’s have a look at the most common ways to open an OFW savings account.

Some banks allow you to open an account while overseas, either through partner banks or their own international branches.

In these cases, you’ll usually need to bring your passport and initial deposit, and complete the application in person.

Other banks offer fully digital applications. This typically involves uploading your ID, taking a selfie, and completing a video verification call.

Some banks can only allow you to open an OFW account if you make a branch visit in person before leaving the Philippines. In this case, you’ll want to get this step completed before you head overseas for your new role, to avoid hassle on arrival.

To open your OFW account in the Philippines, you’ll need to visit your branch with an ID document from the bank’s approved list and complete the application with a staff member.

In most cases, the requirements to open an OFW account in the Philippines include taking along an acceptable ID document and depositing at least the minimum opening deposit amount to complete account registration. While different banks have their own acceptable documents, you can often use:

Many OFW savings accounts work well for holding money in pesos, but they’re not designed for managing money across currencies or sending funds internationally without extra costs.

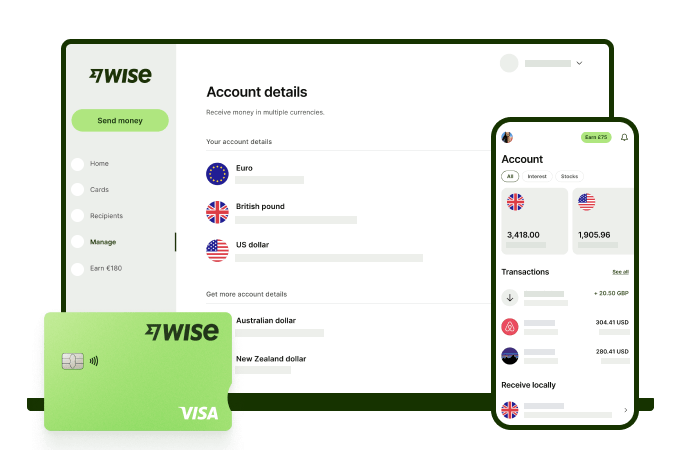

Receive foreign currency and exchange it directly to pesos at the mid-market rate with Wise.

With Wise, you'll get 8+ local account details including PHP, USD, GBP, AUD, and more. This way, you can receive money directly, in a cheap and convenient manner. All you need to get started is to sign up for a free account, and you'll be able to manage your money with just a few taps of your phone.

After getting your money, you can easily convert it to 40+ currencies, with low fees, and the mid-market rate - also known as the rate you see on Google. This includes exchanging to PHP with a one-time conversion fee from 0.57% that's shown upfront, and no markups or additional fees.

Receive, exchange, and move your funds to your local bank account in PHP in a cheap and convenient manner with Wise.

It’s simple and stress free - and lets you keep on top of your finances no matter what you’re up to.

*Please see terms of use and product availability for your region or visit Wise fees and pricing for the most up to date pricing and fee information.

This publication is provided for general information purposes and does not constitute legal, tax or other professional advice from Wise Payments Limited or its subsidiaries and its affiliates, and it is not intended as a substitute for obtaining advice from a financial advisor or any other professional.

We make no representations, warranties or guarantees, whether expressed or implied, that the content in the publication is accurate, complete or up to date.

Learn the PhilHealth contribution for OFWs, including current rates, payment options, how to pay from abroad and how to check your status.

How much is Pag-IBIG contribution for OFWs? Learn rates, benefits, and how to pay your Pag-IBIG contributions online from abroad.

Applying for a BPI credit card as an OFW? Learn the requirements, documents, income rules, and how to apply online from abroad step by step.

Looking for your first credit card? Compare UnionBank credit cards for beginners, including fees, requirements, and how to apply.

Learn how to get a TIN number in the Philippines, including online application steps, requirements, and BIR registration.

Learn how OFW SSS contribution works, including rates, payment methods, and benefits. See the latest SSS contribution table and manage payments easily.