How to Open a Bank Account for Work Permit Holders in Singapore

Learn how work permit holders in Singapore can open a bank account, including requirements, options, and how to receive salary payments.

Pricing claim based on comparative data for select airports and passes. Live pricing is subject to exchange rate fluctuations.

📱Find out how to get lounge access

The GXS Savings Account¹ is a flexible interest-bearing account from local digital bank GXS. GXS offers ways for customers to save with full access to their funds, or to lock away money as a time deposit, to get a higher interest rate. This GXS savings account review covers the GXS interest rate on different savings types and why you might want to open an account.

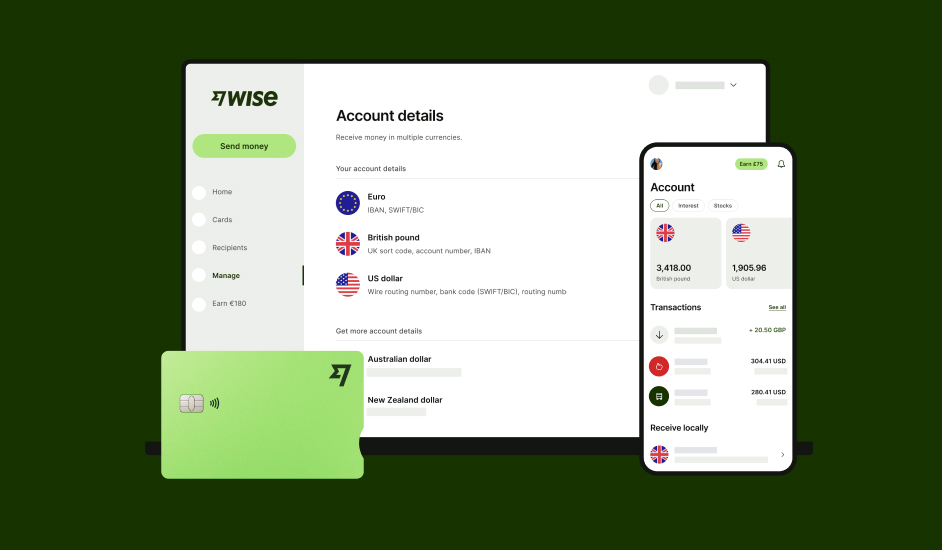

You can also learn more about the Wise card, an easy way to stretch your dollars when paying in foreign currencies.

| Table of contents |

|---|

GXS is a fully licensed Singapore-based digital bank operated through a partnership of Grab and Singtel. The GXS Savings Account is their savings product, which works alongside your main account and GXS debit card, allowing users to save at the same time as spending conveniently on day-to-day items.

GXS Savings Account features include:

Want to compare some Singapore digital banks? Get this review of GXS vs Trust to learn more.

Here are the requirements for opening a GXS account³:

It’s important to note that applications aren’t supported for US citizens, even if they’re legal residents of Singapore.

To meet the legal residency requirement with GSX you’ll need to be a Singapore citizen, Singapore Permanent Resident, or have a valid long-term visa like an Employment Pass (EP).

Here’s how to open a GXS account in a few simple steps:

You may be prompted while applying to upload images of some documents to support your application. If this happens, there will be instructions on your screen, asking you to take a clear photo of some paperwork and upload it for verification. This is a security step and allows GXS to keep your account safe.

Ready to get started? Read our full GXS review, so you know what to expect with your new account.

The GXS interest rates which apply depend on how you use your account. There’s one rate for your core day-to-day account, which comes with your GXS card. You can then move money from this to a Savings Pocket, which is an easy-access vehicle for saving, offering a higher interest rate. Or you can switch your funds into a Boost Pocket, which is a time deposit option that has higher interest again but which does mean you must leave your money for a fixed period of 1, 3, 8 or 12 months.

Here are the current GXS interest rates (18th November 2025) for different GXS savings types:

With GXS, interest is credited daily, which means you can track your earnings easily. Bear in mind that if you withdraw your funds from a Boost Pocket before the term has ended, you will forfeit some interest. There’s also a maximum cap on the amount you can hold across all account types, which varies by customer but will be no more than 95,000 SGD.

To help you decide if the GXS Savings Account is right for you, let's look at some important pros and cons:

| ✅ GXS Savings Account: Pros | ❌ GXS Savings Account: Cons |

|---|---|

|

|

There’s no option to make a local or overseas transfer from your GXS Savings Account to a third party. Your only option is to transfer your balance to your Main Account with GXS and transfer from there.

From your Main Account, you can use your balance to spend with your GXS debit card or to send to another Singapore-based account.

No. You can’t send money directly from GXS to an account in a foreign currency.

From your GXS Savings Account, you can send funds via:

These options are all offered for local SGD payments only.

One very important question before you hand over any money: is GXS bank safe?

The good news is that GXS is a licensed digital bank regulated by the MAS, and your money is therefore protected by the Singapore Deposit Insurance Corporation (SDIC) up to 100,000 SGD in value.

There are no service fees or charges with your GXS Savings Account⁵.

There’s a minimum deposit limit of 100 SGD for each Boost Pocket you open, to a maximum of 85,000 SGD combined across up to 3 pockets.

The other key transaction limit to remember is that your account will have a maximum balance which will be no more than 95,000 SGD, and which may be under this amount. Check your own limits in the GXS app.

The GXS Savings Account is designed for saving and spending in SGD, but it doesn’t support holding foreign currencies or sending money overseas. If you regularly deal with international payments, you may want an additional option.

The Wise account is an easy way to hold and exchange 40+ currencies, including SGD, MYR, EUR, CNY, and more. All you need to do is create a free account to get started.

With Wise, you can exchange currencies at the mid-market rate each time, with low, transparent conversion fees from 0.26% and absolutely no markups. Plus, you can order a linked Wise card for convenient spending without any foreign transaction fees, and free ATM withdrawals up to the value of 100 SGD when you're overseas. You'll even get 8+ local account details to get paid conveniently to your Wise account in SGD and a selection of other major global currencies.

What's more, you can activate Wise Interest to earn returns* on your eligible balances while keeping your money available to spend.

*Growth is not guaranteed. Capital at risk.

Sending money or making payments abroad? Wise also offers fast, low cost transfers to 140+ countries - you can track your transfer in your account and your recipient will also be notified when a transfer reaches them.

No. There’s no minimum deposit amount for GXS savings accounts. You will need at least 100 SGD to open a Boost Pocket, but the main savings account product has no minimum limit.

Sources used:

*Please see terms of use and product availability for your region or visit Wise fees and pricing for the most up to date pricing and fee information.

This publication is provided for general information purposes and does not constitute legal, tax or other professional advice from Wise Payments Limited or its subsidiaries and its affiliates, and it is not intended as a substitute for obtaining advice from a financial advisor or any other professional.

We make no representations, warranties or guarantees, whether expressed or implied, that the content in the publication is accurate, complete or up to date.

Learn how work permit holders in Singapore can open a bank account, including requirements, options, and how to receive salary payments.

A detailed review of the Trust Savings Account in Singapore, covering interest rates, plans, fees, rewards, and who it’s best for.

A detailed review of the Mari Savings Account, including interest rates, fees, limits, cards, transfers, and how to open an account in Singapore.

Learn how to open a POSB bank account for your domestic helper in Singapore. Our guide covers the required documents and step-by-step process.

Comparing GXS and Trust? Read on to find out what a digital bank is, compare features, interest rates, and understand their exchange rates

Planning on opening a DBS multi-currency account in Singapore? Read this comprehensive guide on everything you need to know before