RCBC OFW Savings Account: Benefits, Requirements & How to Open

Learn how to open an RCBC OFW savings account, including requirements, fees, benefits, and how to send money to the Philippines.

| ⚠️ Update: Effective 8 September 2025, SeaBank is now officially known as MariBank. This article has been updated to reflect this change, though some historical references to "SeaBank" may remain. |

|---|

If you need an account to save and earn interest - or a debit card for easy spending at home and abroad - you could get what you need from either CIMB¹ or Maribank (formerly SeaBank)². Both offer secure, convenient account and card services - but the scope of CIMB vs MariBank is quite different in many ways.

This guide walks through the services, features, and fees of MariBank vs CIMB so you can decide which is better - CIMB or MariBank - based on your specific needs. We'll also introduce the Wise account, a handy companion to make your money go further with low, transparent fees.

| Table of contents |

|---|

Sign up for a free account now

MariBank and CIMB are not the same company.

MariBank is part of the group behind Shopee, and offers savings accounts, loans and a debit card. It’s licensed and regulated in the Philippines, but its range of products is quite focused and aimed at personal customers only. We'll also introduce the Wise account, a handy companion to make your money go further with low, transparent fees.

CIMB on the other hand is a large bank, operating across the Philippines and many other countries across the region, with a very broad range of accounts and services for personal and business customers.

Whether MariBank or CIMB are better for you will depend on the features you need and the type of transactions you want to make. This guide will help you decide.

MariBank is owned by Singapore based company Sea Limited. Sea Limited is also the owner of e-commerce site Shopee and game developer Garena. When it comes to finance, MariBank aims to help connect Filipino customers with accounts, loans and card services you can access with just a phone or laptop.

CIMB stands for Commerce International Merchant Bankers, and is a Malaysia headquartered bank which operates throughout the Southeast Asia region. CIMB has a range of account and card services in the Philippines and also works with major partners such as GCash to offer tailor made products for the local market. Available services include savings accounts, debit cards, loans and credit cards.

The products available from MariBank and CIMB are quite different, and so ultimately the right option for you might simply come down to the exact services you require. Both offer savings accounts with a card for spending, and also have some options for earning cashback, but the CIMB suite of products is more comprehensive than the range of financial services available from MariBank in the Philippines.

Here’s an overview of MariBank vs CIMB head to head on feature availability:

| Feature or service | CIMB | MariBank |

|---|---|---|

| Eligibility | At least 18 years old, Filipino citizen, non US person | At least 18 years old, Filipino citizen or resident US persons need an SSN |

| Saving accounts | Available - Fast Plus Savings account, Up Save account, time deposits, and other savings options | Available - Savings account |

| Maximum available interest rate | 0.75% for Fast Plus account³ 2.5% for Up Save account⁴ 5.25% for MaxSave time deposit account⁵ | 3.5%⁶ |

| Debit cards | Available | Available |

| Credit cards | Available - REVI credit | Not available |

| Cash back on card spending | Available | Available |

| Local payments | InstaPay andPESOnet | InstaPay andPESOnet |

| International payments | Available via remittance partners⁷ | Not available |

| Credit facilities | Available - loans, credit, buy now, pay later, credit cards | Available - loans for select customers only |

| Business services | Available for MSMEs⁸ | Not available |

| Regulated and PDIC insured | Yes | Yes |

*Details correct at time of research - 29th August 2025

If you’re thinking of opening a savings account you can use day-to- day, with no limits on the number of withdrawals you can make, either CIMB or MariBank may have a product to suit you.

MariBank’s savings account has a flat rate of interest set at 3.5% for deposits of up to 1 million PHP, with a slightly lower rate of 3% over that amount. You get a card with your account and can spend freely - making this a convenient option for flexible money management.

CIMB has a selection of savings products, including some with and without a linked card, and some time deposit products which do not allow you to withdraw your money without penalty. Which is the best for you might depend on your specific needs. We’ll examine the MariBank vs CIMB core savings accounts, and their interest rates, next so you can see if either is a good fit.

MariBank has only one account for savings, while CIMB has several different savings account products, including the Fast Plus account and the Up Save account, and various time deposit options.

We’ve selected the Fast Plus account to review here as it offers a handy debit card and ways to send local and international transfers. The Up Save account as a comparison does offer higher interest but has no debit card, which makes it less suited to daily use. We’ll take a look at different CIMB savings products and the CIMB interest rates available in a moment.

First, an overview of the MariBank vs CIMB saving account options.

| Feature or service | CIMB Fast Plus⁹ | MariBank |

|---|---|---|

| Opening fee | No fee | No fee |

| Minimum balance | No minimum balance | No minimum balance |

| Maintenance fee | No fee | No fee |

| Base interest | 0.75% | 3.5% |

| Debit card available | Yes | Yes |

| Local transfer fee | No fee | 15 transfers/week free, then 15 PHP |

| International transfer fee | Remittance fees depend on the partner you send with | Not available |

*Details correct at time of research - 29th August 2025

The MariBank vs CIMB interest rate you get will depend on the product you select.

MariBank only offers one savings account option which has an interest rate of 3.5% for deposits of up to 1 million pesos. If you save more than that, the interest you earn on the excess amount will be set to 3%¹⁰.

CIMB on the other hand has several different account products for savers, which all have their different interest rates. Here’s a comparison of the account options available from CIMB:

| Interest rate | Features | |

|---|---|---|

| CIMB Fast Plus | 0.75% | Debit card available |

| CIMB Up Save | 2.5% | Cash in and cash out at partner locations in case |

| CIMB Max Save | Up to 5.25% depending on term | 5,000 PHP minimum deposit - time deposit account |

| CIMB Grow | 4%¹¹ | By invitation only - for customers without Gsave accounts |

| CIMB GSave | 2.6%¹² | Partnership with GCash |

*Details correct at time of research - 29th August 2025

The MariBank savings account offers a linked debit card for spending. CMB has a debit card which is linked to your Fast Save account and also offers a credit card option.

Both of these cards do offer a good way to get access to your money while still earning interest on the funds you hold. However, there are also some fees you’ll need to consider - particularly if you decide to use your card abroad. While both MariBank vs CIMB issue cards on global networks which you can use more or less anywhere, there are fees of 2% - 3% for international spending.

Here’s a summary of the MariBank and CIMB card fees you’ll need to know about:

| Feature or service | CIMB Fast Save Card | MariBank Debit Card¹³ |

|---|---|---|

| Card order fee | 300 PHP | 99 PHP |

| International usage | Available globally anywhere network is accepted | Available globally anywhere network is accepted |

| ATM fee | Waived for CIMB and in network ATMs | 15 PHP |

| International ATM fee | Set by ATM operator | No fee |

| Foreign transaction fee | 3% | 2% |

| Virtual card available | Yes | Yes |

| Cashback options | Yes | Yes |

*Details correct at time of research - 29th August 2025

Make seamless foreign currency payments and transactions with low fees and the mid-market rate with Wise.

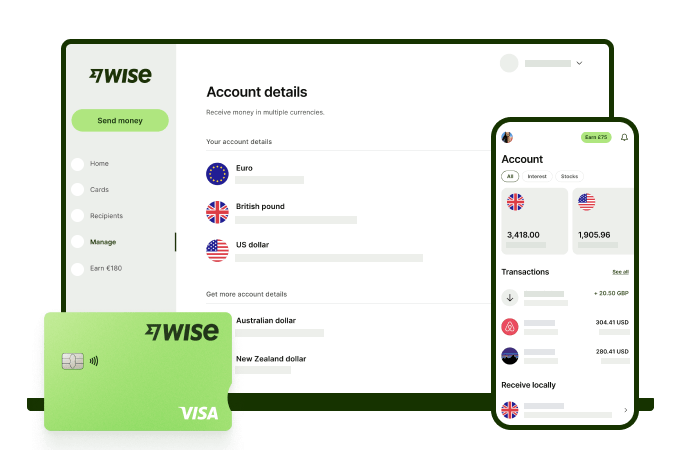

The Wise account is an easy way to hold and exchange 40+ currencies, including PHP, USD, CNY, and more. All you need to do is create a free account to get started.

With Wise, you can exchange currencies at the mid-market rate each time, with low, transparent conversion fees from 0.57% and absolutely no markups. Plus, you can order a Wise card for convenient spending at the same great rate, without any foreign transaction fees.

In supported countries, you can also use Wise to pay with QR codes, which means you can pay like a local without needing cash or a separate local wallet. This can be especially handy when you're travelling in places where QR payments are widely accepted.

At times you need cash, you can also make up to 2 free ATM withdrawals to the value of 12,000 PHP when you're overseas. You'll even get 8+ local account details to get paid conveniently to your Wise account in PHP and a selection of other major global currencies.

Sending money or making payments abroad? Wise also offers fast, low cost transfers to 140+ countries - you can track your transfer in your account and your recipient will also be notified when a transfer reaches them.

Get the most out of every peso and save more when you use Wise.

Sources:

*Please see terms of use and product availability for your region or visit Wise fees and pricing for the most up to date pricing and fee information.

This publication is provided for general information purposes and does not constitute legal, tax or other professional advice from Wise Payments Limited or its subsidiaries and its affiliates, and it is not intended as a substitute for obtaining advice from a financial advisor or any other professional.

We make no representations, warranties or guarantees, whether expressed or implied, that the content in the publication is accurate, complete or up to date.

Learn how to open an RCBC OFW savings account, including requirements, fees, benefits, and how to send money to the Philippines.

Compare the best banks in the Philippines for 2026. See fees, ATM access, savings options and international services to find the right bank for you.

A step-by-step guide to the Dubai tourist visa for Filipinos, covering requirements, visa types, costs, validity, and how to apply in 2026.

Working abroad or getting paid in foreign currency? Learn about the Metrobank OFW Savings account requirements and options to receive and remit money.

Working abroad or getting paid in foreign currency? Learn about the PNB OFW Savings account requirements and options to receive and remit money.

Are you an OFW looking for a BPI savings account? Learn about the requirements, fees, how to open an account online, and remittances.