Understanding Stripe Transfer and Transaction Limits (2026)

Discover everything you need to know about Stripe transfer and transaction limits. Maximize your payments with our easy-to-understand guide

Buy Now, Pay Later (BNPL) services can increase conversion rates and average order values. By offering customers flexible payment options, businesses can reduce the friction of up-front costs.

Klarna and Sezzle are two leading BNPL providers in the US. While both help businesses secure more sales, they have key differences in their product offerings, fee structures, and ideal business partners. This guide compares Klarna vs. Sezzle from a business perspective to help you choose the right partner for your company. We'll also discuss the Wise Business account. The global account that can help your company with all things cross-border.

Do you send and receive global payments?

Wise Trustpilot Score: 4.3 stars on 230,000+ reviews

No minimum balance requirement and no monthly fees

Integrates with QuickBooks, Xero, Sage, and more

| Klarna | Sezzle | |

|---|---|---|

| Key Features | Multiple payment options: Pay in 4, Pay in 30 days, long-term financing.1 | Simple "Pay in 4" plan over 6 weeks.1 |

| Main Fees | Custom-quoted for merchants. A typical rate is around 5.99% + 0.30 USD per transaction.6 | Custom-quoted for merchants. A typical rate is around 6% + 0.30 USD per transaction.7 |

| Great For | Mid-market to large businesses with a wide range of product prices.4 | Small to medium-sized businesses looking for a straightforward BNPL solution.4 |

Understanding the core products of each provider is the first step in deciding which one fits your business and customer base.

Klarna provides a suite of flexible payment solutions for customers. This variety allows businesses to offer different options based on the order value.

This range of options makes Klarna a versatile choice, particularly for businesses with diverse product catalogs and price points. It is often favored by larger retailers.5

Sezzle focuses on a single easy-to-understand payment structure. Its primary offering is designed for simplicity for both the business and the consumer.

Pay in 4: Customers pay for their purchase in 4 interest-free installments over 6 weeks. The first payment is made at the time of purchase.4

This straightforward approach is often a good fit for small and medium-sized businesses that want to offer a simple BNPL option without the complexity of multiple financing plans.2

For a business, the most critical factor is the merchant fee. This is the cost you pay to the BNPL provider for every transaction. These fees directly impact your profit margins.

Klarna's pricing is customized for each merchant. The final fee depends on your business's size, sales volume, and industry. However, a typical fee structure is a percentage of the transaction value plus a fixed fee.

For example, a common rate is around 5.99% + 0.30 USD per transaction.6 On a 200 USD sale, your business would pay a fee of approximately 12.28 USD to Klarna.

Similar to Klarna, Sezzle provides custom pricing for its business partners. The fee is also a combination of a percentage and a fixed amount per sale.

A typical rate for Sezzle is around 6% + 0.30 USD per transaction.7 On the same 200 USD sale, the fee would be approximately 12.30 USD. While the difference appears minor, it can become significant over thousands of transactions.

If your business sells to customers outside the US, receiving payouts can introduce currency conversion costs. When a BNPL provider settles a transaction in a foreign currency and transfers it to your USD bank account, the exchange rate used can affect your bottom line.

Neither Klarna nor Sezzle publicly detail their specific foreign exchange (FX) markups for merchant payouts. Businesses should clarify these costs during the onboarding process, as they are a hidden factor in the total cost of using a BNPL service for cross-border sales.

The best choice between Klarna and Sezzle depends on your business model, customer base, and operational preferences.

For a business with a wide range of prices, Klarna's multiple options provide a tailored checkout experience. For a business prioritizing a simple, low-maintenance solution, Sezzle's focused approach is often a better fit.

After implementing a BNPL solution like Klarna or Sezzle, your business may see a rise in sales, including from international customers. Managing these cross-border payments efficiently is the next step in optimizing your financial operations.

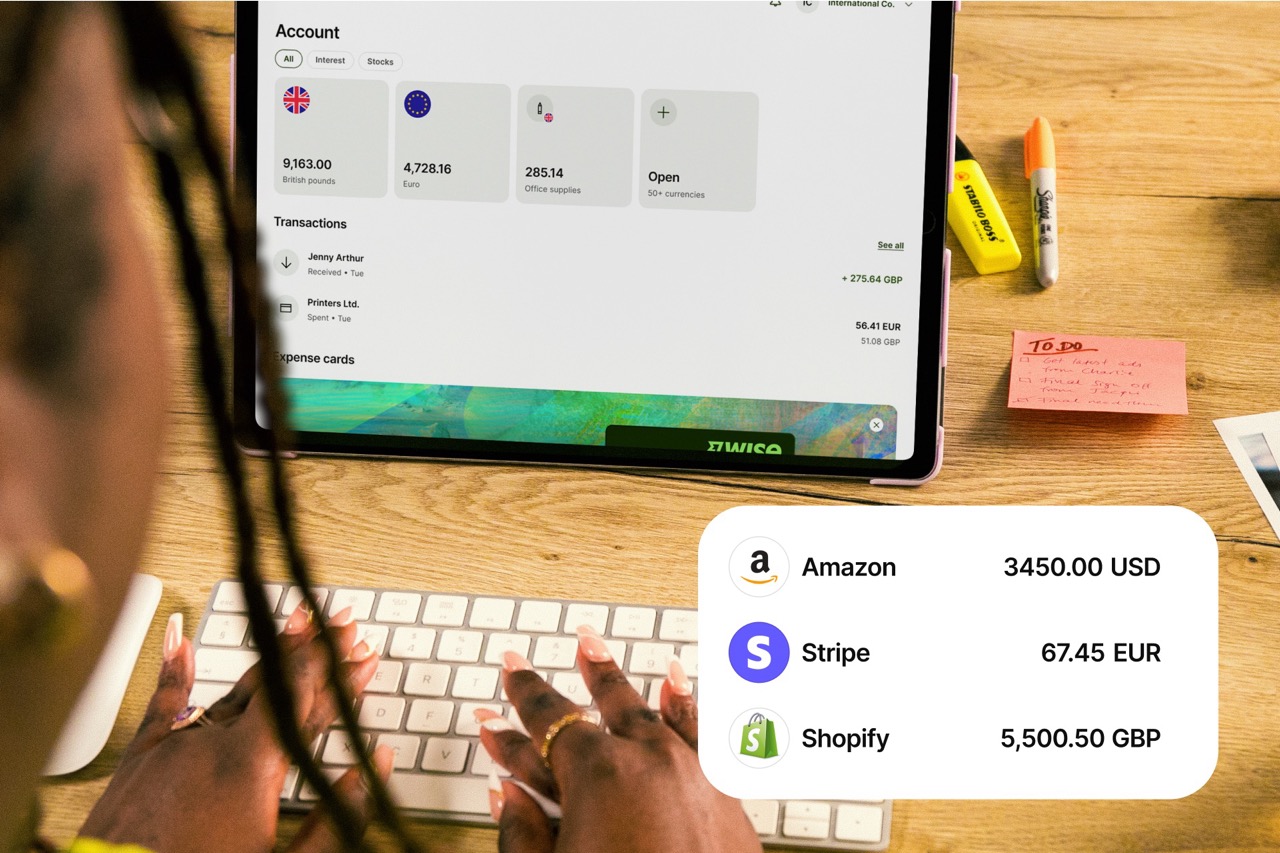

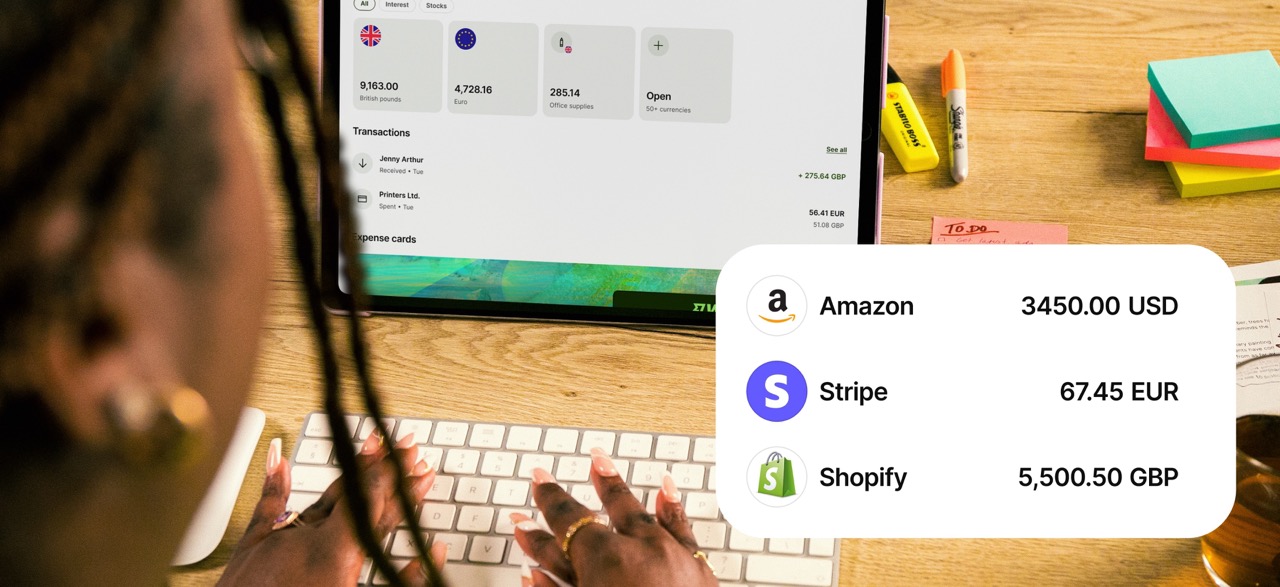

When you receive payouts in foreign currencies, traditional banks often apply a markup to the exchange rate, cutting into your revenue. The Wise account offers a solution. It provides you with local bank details in major currencies like EUR, GBP, AUD, and more. This allows you to receive payments like a local, bypassing high conversion fees.

With a Wise Business account, you can hold funds in over 40 currencies and pay international suppliers or contractors at the mid-market exchange rate with a single transparent fee. This ensures that the profits you earn from global sales are not lost to hidden bank fees, complementing the growth driven by your BNPL partner.

Which is better for a small business: Klarna or Sezzle?

Sezzle is often considered a strong choice for small businesses due to its simple "Pay in 4" model and focus on the SMB market.2

What are the main differences between Klarna, Sezzle, and Afterpay?

The main differences are in their payment options and target markets. Klarna offers the most diverse plans (Pay in 4, Pay in 30, financing).1 Sezzle and Afterpay primarily focus on a simple "Pay in 4" structure, though their repayment schedules can differ slightly.

Do businesses pay a fee for Klarna and Sezzle?

Yes. Both Klarna and Sezzle charge merchants a fee for every transaction. This fee is typically a percentage of the sale amount plus a small fixed fee.6

Is Klarna or Sezzle better for high-ticket items?

Klarna's long-term financing options may be better suited for businesses selling high-ticket items, as it allows customers to spread payments over a longer period, potentially with interest.1

Wise is not a bank, but a Money Services Business (MSB) provider and a smart alternative to banks. Wise makes it easy to send, hold, and manage business funds in 40+ currencies. You can get major currency account details for a one-off fee to receive overseas payments like a local. Simply add the local account details when billing international customers to receive international payments with no fees.

Account opening is 100% online, with no need to visit a branch or book appointments.

Once you’re set up, you can connect to software such as Wave, FreshBooks, and more. You can also withdraw funds from Stripe without currency conversion fees.

Open a Wise Business account online

| Some key benefits of Wise Business include: |

|---|

|

Sources:

*Please see terms of use and product availability for your region or visit Wise fees and pricing for the most up to date pricing and fee information.

This publication is provided for general information purposes and does not constitute legal, tax or other professional advice from Wise Payments Limited or its subsidiaries and its affiliates, and it is not intended as a substitute for obtaining advice from a financial advisor or any other professional.

We make no representations, warranties or guarantees, whether expressed or implied, that the content in the publication is accurate, complete or up to date.

Discover everything you need to know about Stripe transfer and transaction limits. Maximize your payments with our easy-to-understand guide

Discover the key differences between Klarna and PayPal for businesses. Explore features, fees, and benefits to choose the best payment option for your needs.

Compare Klarna vs. Affirm to help you decide which is a better fit for your business. Explore fees, features, products, and more.

Get a comprehensive review of Shopify Plus for global expansion, including key features, pricing, and best practices

Explore embedded payments and how integrating payment functionality directly into your software can enhance user experience and streamline transactions.

What is Meta Pay? Get a breakdown of Meta's digital wallet and payment solutions for a fast and secure checkout experience.