Travel Better: Airport Lounge Passes Are on Wise

We are thrilled to announce that Wise cardholders can now purchase airport lounge passes directly through the Wise app.

If you live in Spain or have a Spanish bank account, check if your bank is following the rules and tells you exactly how much you’ll pay for your cross-border payment.

Join our cause to spread the word and make sure we hold banks to account and get EU rules enforced across the Continent.

Today, transparent cross-border payments are a right protected under EU law.

The problem is that some banks still aren’t playing by the rules, taking advantage of the fact that most European consumers aren’t aware of their rights under new rules, which came into force in April 2020.

To check whether this was the case in Spain, we had a look at six Spanish banks (BBVA, Abanca, Openbank, Santander, ING Spain and Cajamar).

A few years ago, we spent a lot of time talking about the Cross Border Payments Regulation 2 (CBPR2) at Wise. This new law requires providers to show customers “all currency conversion charges” (a.k.a. any transaction fees - so-called upfront fees - and the exchange rate mark-up) before you make a cross-border payment. The goal is to increase transparency for consumers making cross-border payments between EU countries, for example sending money from Spain to Hungary.

We checked whether banks in Spain were applying European rules, and it doesn’t look like that’s the case.

Calculating the price of an international transfer should be as simple as that:

Mid-market (real) exchange rate + transfer transaction fee (to cover costs and, perhaps, a profit) = what should be paid

Banks purposely make it hard to understand the exchange rate, the transaction fee and the exchange rate mark-up. Unfortunately, that’s still far too common in Spain.

The real, mid-market exchange rate is what most people google. It’s provided by independent sources like Reuters or Bloomberg. And you can check the mid-market rate for a specific day (rather than live) on the European Central Bank (ECB)’s website too. While this doesn’t always reflect the exchange rate of that specific moment in time, it will still give you a pretty good indication of the ‘right’ rate. But many banks inflate that exchange rate by adding a mark-up. But they’ll never tell you that what you’re getting isn’t actually the real exchange rate and you’re getting a bad deal.

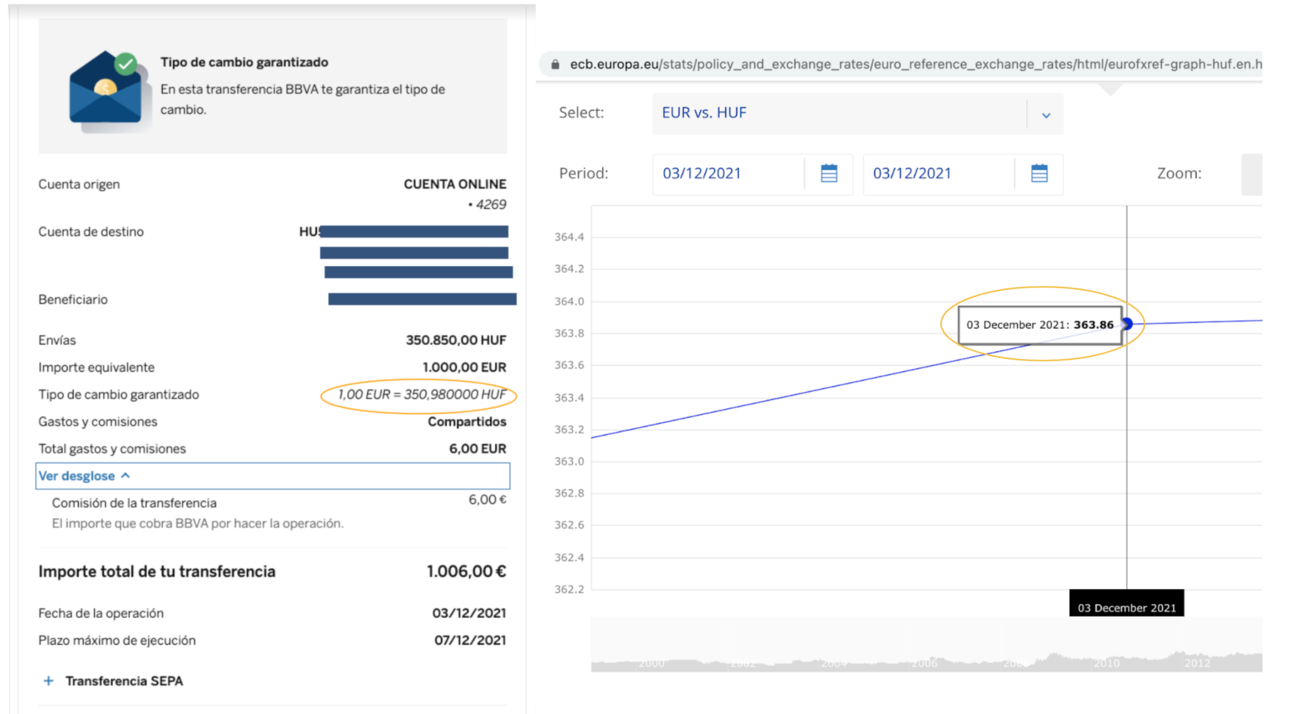

Here is an example of how many Hungarian forints you would get for € 1,000. On the left is the BBVA exchange rate (€ 1 = 350.98 HUF) and on the right is the mid-market exchange rate (€ 1 = 363.86 HUF) offered by the ECB.

Showing the mid-market (real) exchange rate is important, so customers don’t need to resort to complicated mental maths to calculate how much they’re being charged. But if a bank doesn’t use the real exchange rate, which one does it use?

Well, their own rate. And each bank has a different way of communicating the exchange rate they use (if at all).

The result of all that unnecessary complexity is that consumers don’t know how much they’re overpaying for a money transfer.

This is how much HUF you'd get for € 1,000, based on the example above.

| BBVA | ECB | |

|---|---|---|

| Exchange rate applied | 350.98 | 363.86 |

| How much you get for € 1,000 | 350,850 HUF | 363,860 HUF |

This means that a customer loses 12,880 HUF (over € 35.4):

363,860 HUF - 350,980 HUF = 12,880 HUF

These € 35.4 are equivalent to the mark-up BBVA hides in their exchange rate. Unfortunately, most people are not aware of these hidden fees.

In short, many Spanish banks are not transparent, because they overcharge their customers through inflated exchange rates that hide a mark-up.

At Wise we wanted to put ourselves in a customer's shoes. For example, how much money would a Spanish Erasmus student be losing when sending € 1,000 to pay their tuition fees in another EU country?

So we sent € 1,000 to Hungarian forints, Danish kroner and Polish zlotys from some Spanish bank accounts. This is what we found:

| Exchange rate applied (EUR / HUF-DKK-PLN) | Real exchange rate (EUR / HUF-DKK-PLN) | Hidden fee, amount lost by a customer that sends € 1,000 (% mark-up on the exchange rate) | Transfer fee, reported by the bank | Total fee for a € 1.000 transfer | |

|---|---|---|---|---|---|

| BBVA | 350.98 HUF | 363.86 HUF | € 35.4 (3.67%) | € 6 | € 41.4 |

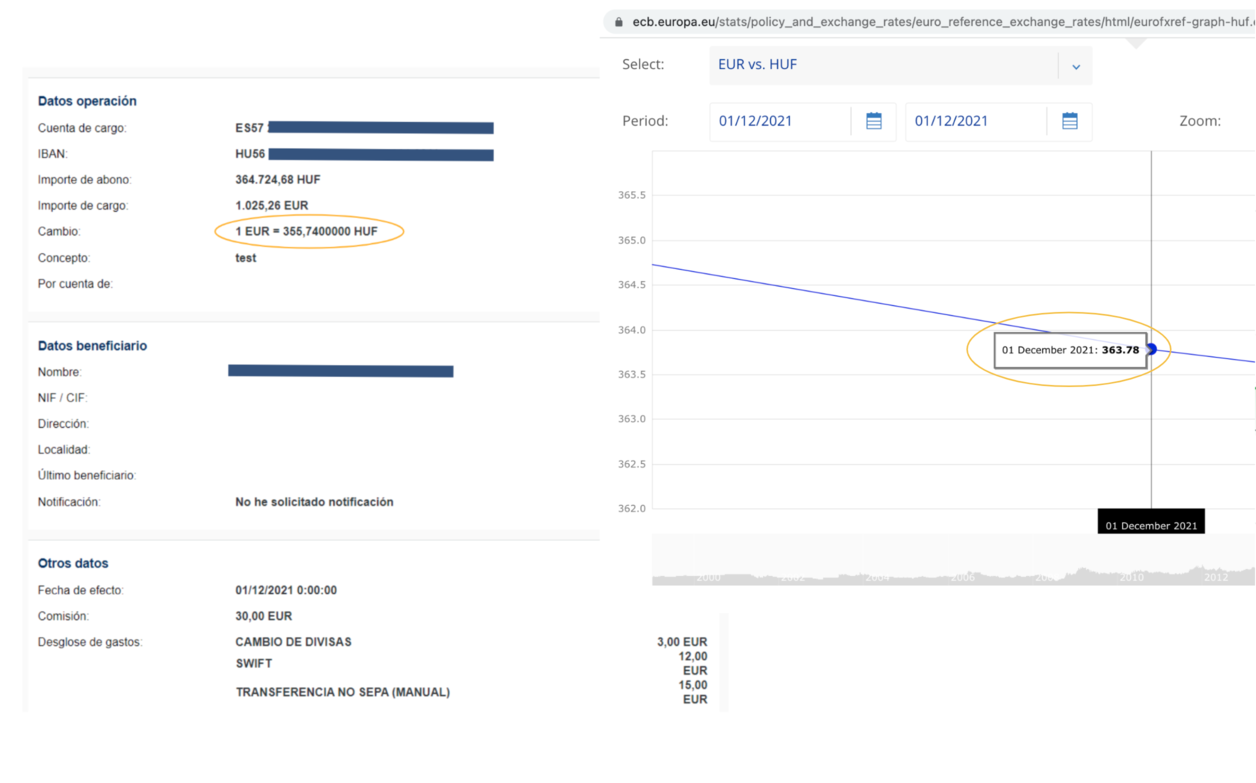

| Abanca | 355.74 HUF | 363.78 HUF | € 22.1 (2.26%) | € 30 | € 52.1 |

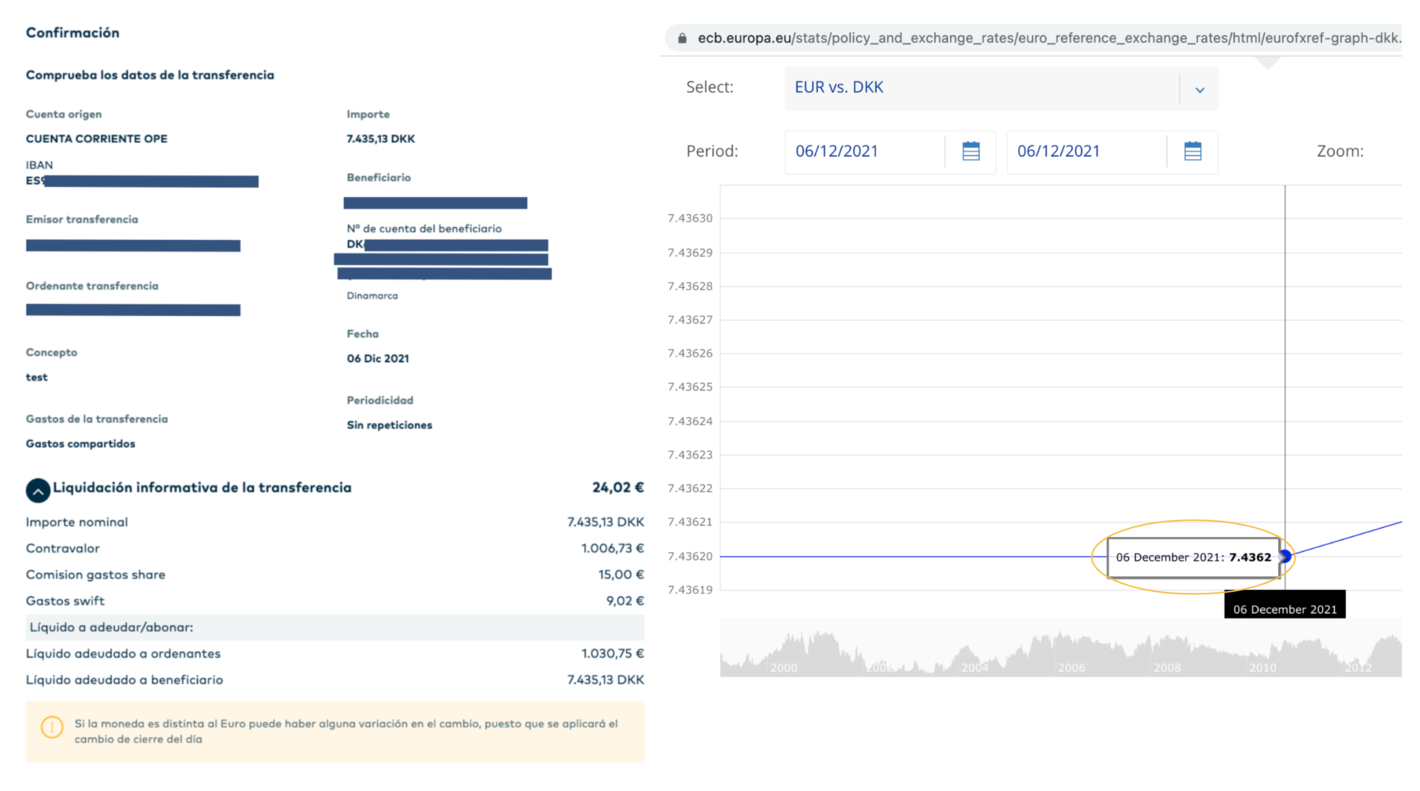

| Openbank | 7.386 DKK | 7.4362 DKK | € 6.75 (0.68%) | € 24.02 | € 30.77 |

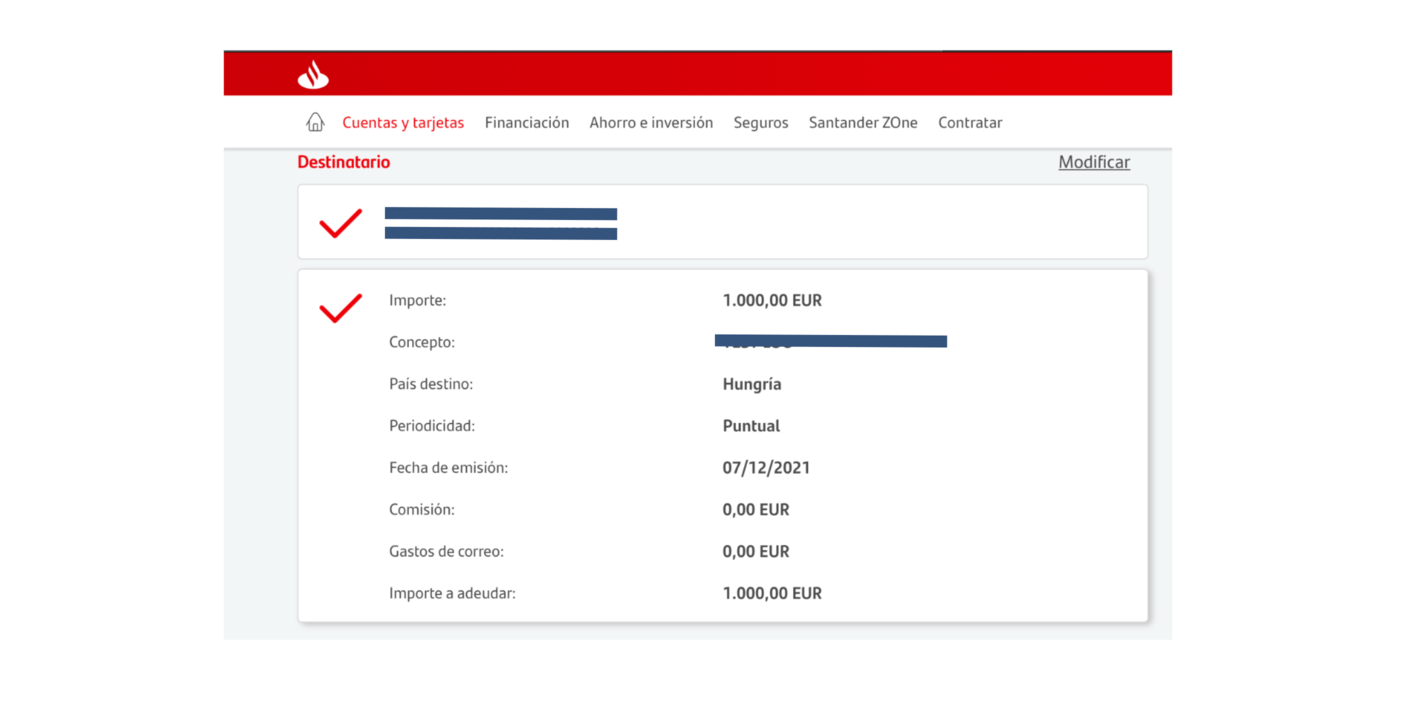

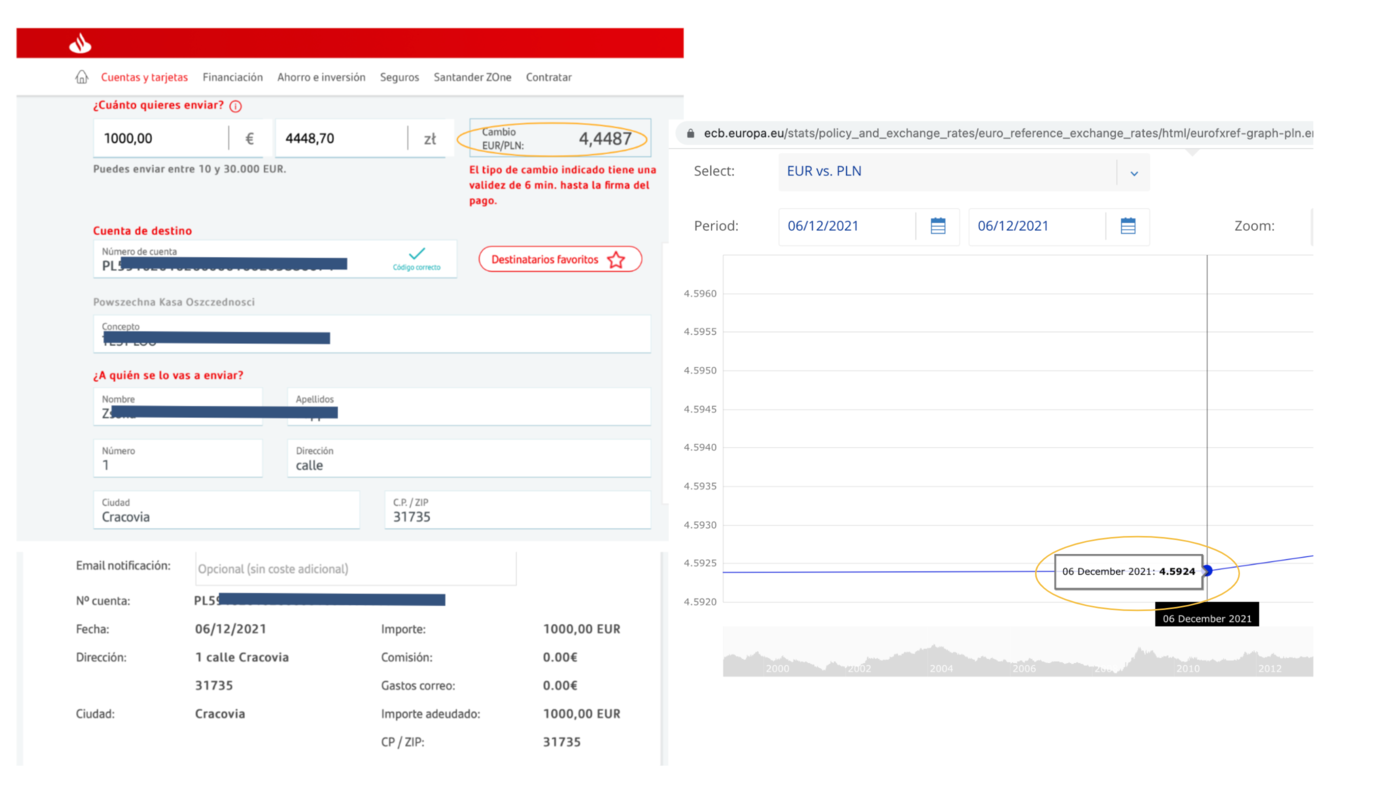

| Santander | 4.4487 PLN | 4.5924 PLN | € 31.30 (3.23%) | € 0 | € 31.3 |

| ING Spain | ING Spain is the only bank on this list which explicitly communicates the currency conversion fee as a cost (“2% of the daily exchange rate set by the ECB”), aside from the transaction fee (€ 15) | € 35 | |||

| Cajamar | 355.63 HUF | 362.44 HUF | € 18.8 (1.92%) | € 3.82 | € 22.62 |

Abanca warned us about their transaction fees, both on the first and the confirmation screen (€ 30 in total).

They also showed us the exchange rate used in the transaction. But it doesn’t correspond to the mid-market rate, it’s inflated by 2.26%. And that mark-up is not communicated as a cost at the time of the transfer.

Openbank, Santander Group's digital bank, made it even harder. Even though they communicated the transaction fee (€ 24) and the “total amount” to be paid, they didn’t show the exchange rate used.

So we had to do the calculations again:

If we pay € 1,006.63 for DKK 7,435.13, the exchange rate used is € 1 = DKK 7.386

If we compare this exchange rate to the real one, we can see that Openbank adds a 0.68% surcharge, which they fail to communicate as a cost.

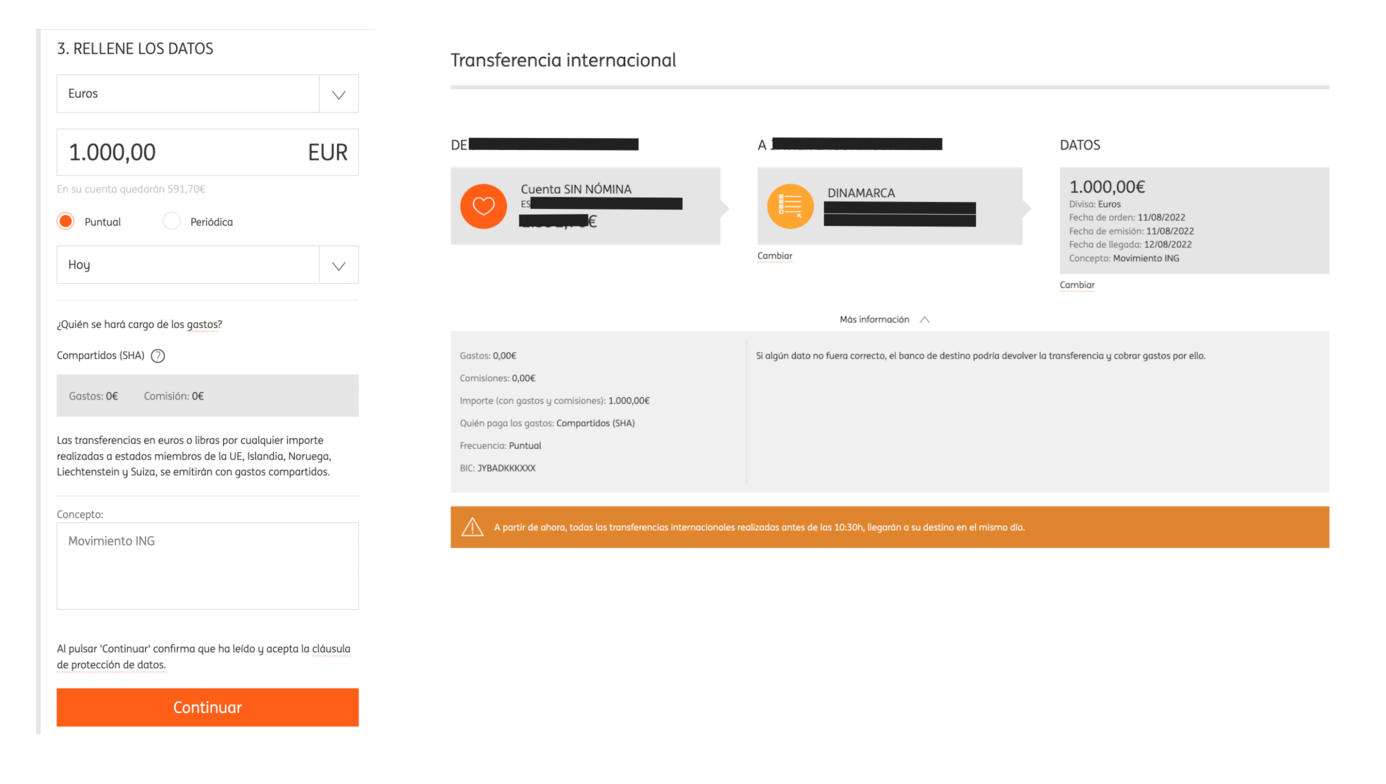

Let's move on to Openbank's parent company. First, we try to make a SEPA transfer from Euro to Hungarian forint, but Santander only allows sending Euro by default. What happens to the money on the other side? Will the receiving bank convert it? How much will my recipient end up with? How can I check that it really is a "zero-fee" transfer?

Next we tried transferring euros to Polish zlotys, also advertised as "zero fee". To send Polish zlotys, instead of a SEPA transfer, for some reason you have to follow the same procedure as for sending US dollars or Mexican pesos...

In this case, Santander does include the exchange rate used, but like most other banks, this doesn’t correspond to the mid-market rate. In fact, they’ve included a 3.23% surcharge which is not communicated to the customer as a cost.

We couldn’t find any information on how Santander calculates their exchange rates. But we did find the paragraph below, where they refer to the "profit margin" on currency exchanges.

When sending Euros to Danish krones with ING Spain using the default payment flow, there was no information about the exchange rate applied or the total amount the recipient will get, just the confirmation. It’s likely that the recipient’s bank will be converting the EUR to DKK, but it’s impossible to know what the exchange rate is and how much the recipient will get.

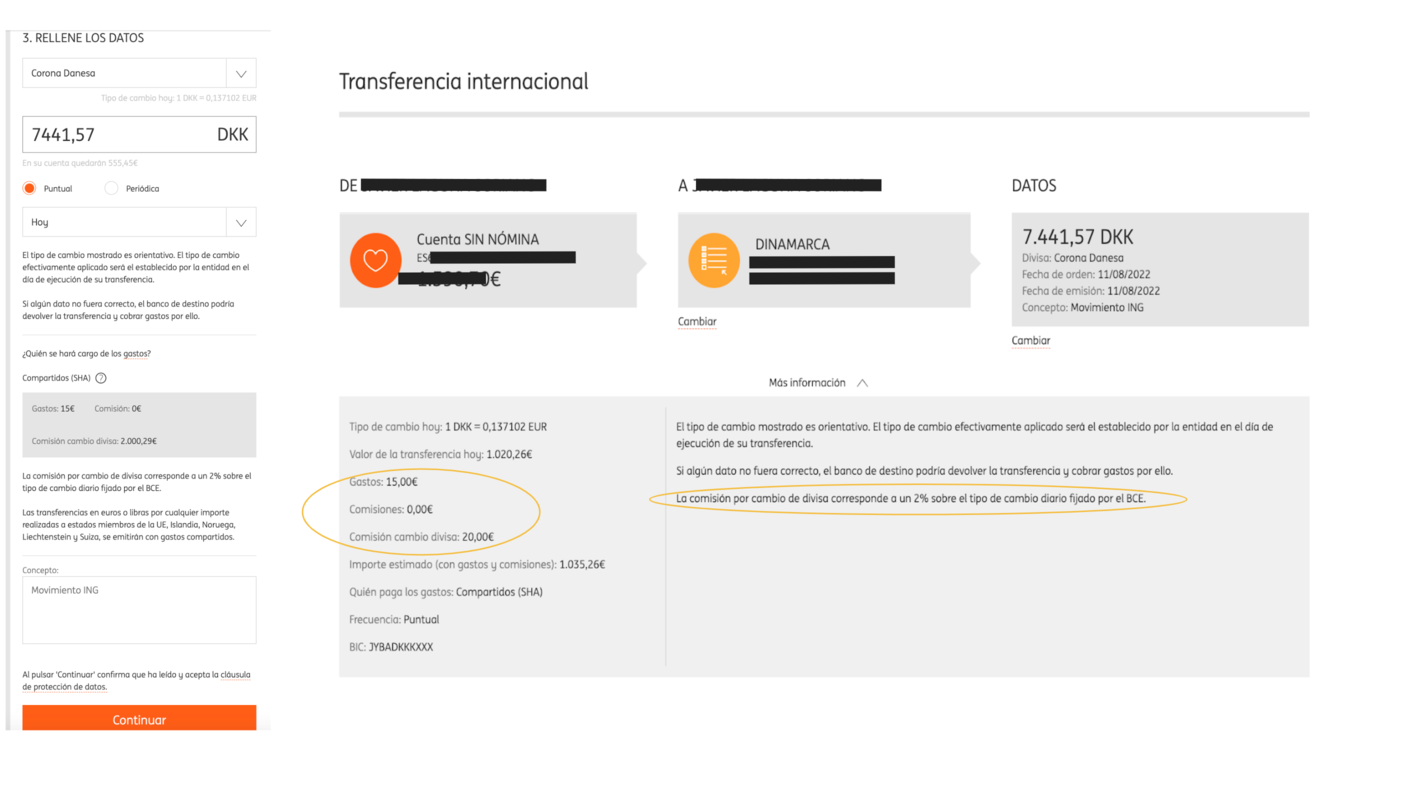

Choosing a different payment flow allows us to send Danish krones, instead of Euros. In this case, we have to celebrate that ING Spain explicitly mentions the currency conversion fee as a cost, aside from the transaction fee: “The foreign exchange fee corresponds to 2% of the daily exchange rate set by the ECB”.

This transparent approach fulfils the spirit of the law, and ensures consumers understand the total cost of what they’re paying, before making the payment. We’re excited to see ING leading the way in Spain when it comes to transparency.

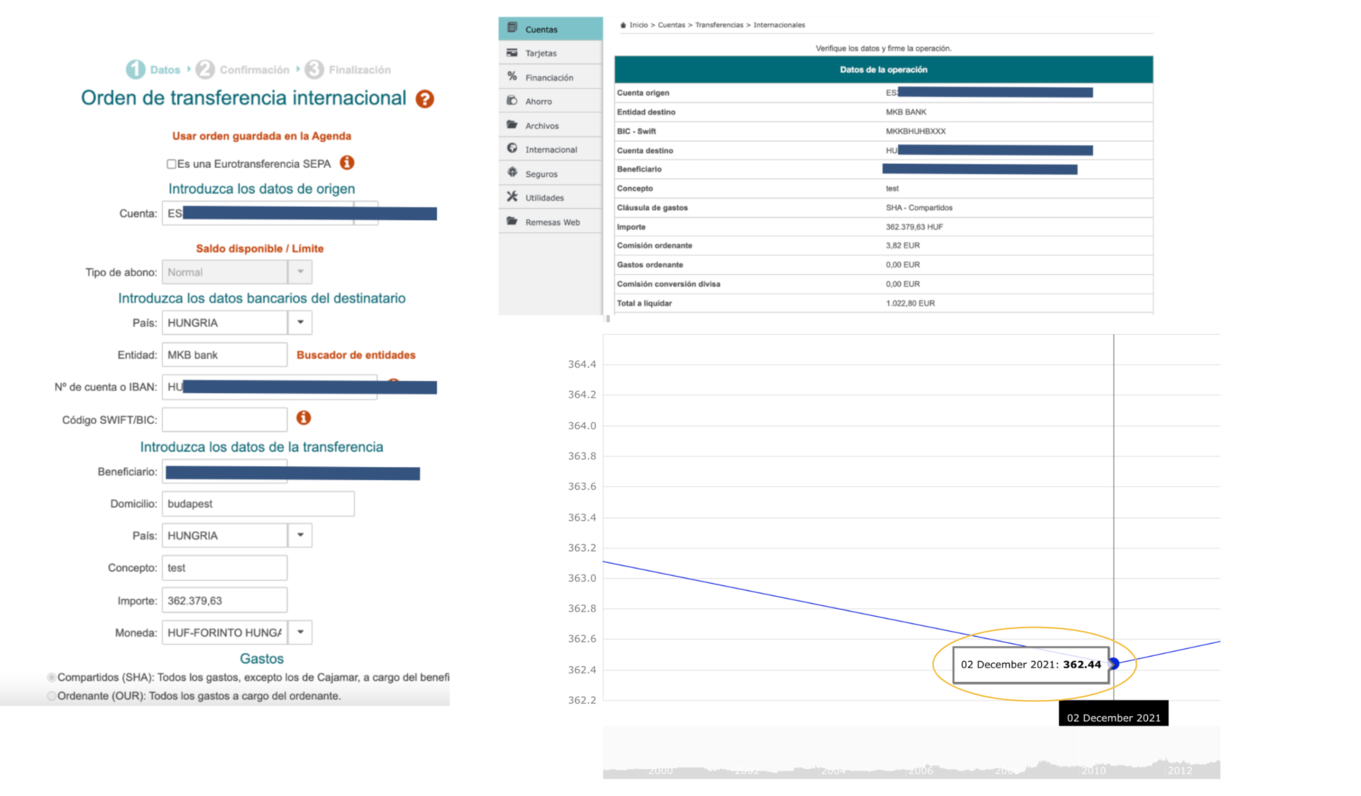

Cajamar’s performance was in the same vein. Again, we tried to transfer Euro to Hungarian forints and, to our surprise, it’s the customer who has to choose whether this is a SEPA transfer or not...

If the customer doesn’t notice this detail and continues with the transaction, the following happens: Cajamar reports the total price for the transaction and the transfer fee. Again, no trace of the exchange rate applied.

So we will have to do our own maths again:

Total amount € 1,022.8 - Transfer fee € 3.82 = cost of currency exchange € 1,018.98

If we pay € 1,018.98 for 362,379.63 HUF, the exchange rate is € 1 = 355.63 HUF

Turns out that Cajamar added a 1.92% mark-up to the exchange rate, without informing the customer.

But what if we had ticked the SEPA transfer field? Like Santander, Cajamar only allows you to send Euros by default. So when will the money be converted? And how can you check that the exchange rate applied corresponds to the real, mid-market one?

At this point, it should come as no surprise that other banks are skirting the rules set by the EU. Hidden fees in exchange rate mark-ups allow banks to remain in breach of transparency rules.

In a single year, Europeans lost up to 12.5 billion euros when spending or sending money abroad. Increased transparency should lower this amount, but if banks aren’t being held accountable, nothing will change.

If you live in Spain or have a Spanish bank account, check if your bank is following the rules and tells you exactly how much you’ll pay for your cross-border payment.

Join our cause to spread the word and make sure we hold banks to account and get EU rules enforced across the Continent.

Methodology: Euro foreign exchange reference rates provided by the European Central Bank –reference rates are based on a regular daily concertation procedure between central banks across Europe, which normally takes place at 14:15 CET.

*Please see terms of use and product availability for your region or visit Wise fees and pricing for the most up to date pricing and fee information.

This publication is provided for general information purposes and does not constitute legal, tax or other professional advice from Wise Payments Limited or its subsidiaries and its affiliates, and it is not intended as a substitute for obtaining advice from a financial advisor or any other professional.

We make no representations, warranties or guarantees, whether expressed or implied, that the content in the publication is accurate, complete or up to date.

We are thrilled to announce that Wise cardholders can now purchase airport lounge passes directly through the Wise app.

Our journey towards instant payments We’ve been working behind the scenes to make transfers faster and our delivery estimates more accurate. Now, 75% of...

Sending money to Estonia? Use the new Viitenumber field and AI invoice scanning to make your transfers to Estonia faster, easier, and perfectly matched.

At Wise, our vision is money without borders. In order to build the future of global money, we need a team that’s as diverse as the customers we...

Got an invoice to pay? A screenshot of someone's bank details? A QR code? Scan it, photograph it, or upload it — Wise reads the details and sets up the transfer

We're thrilled to introduce a powerful new feature designed to save you time and eliminate the frustration of manual data entry when sending money. Now,...