Best savings accounts for non-UK residents

Read our roundup of the best savings accounts for non-UK residents, including options from Barclays, HSBC Expat, NatWest and Skipton International.

We’re well past the days of having to visit a bank branch in person just to open a bank account. In the UK, both high street banks and digital-only upstarts now let you get an account entirely online. With some banks, you can even take care of the whole process on an app in under 15 minutes.

In this guide, we’ll walk through how to open a bank account online. We’ll go over your options, the steps involved, the documents you’ll need, and fees to watch out for.

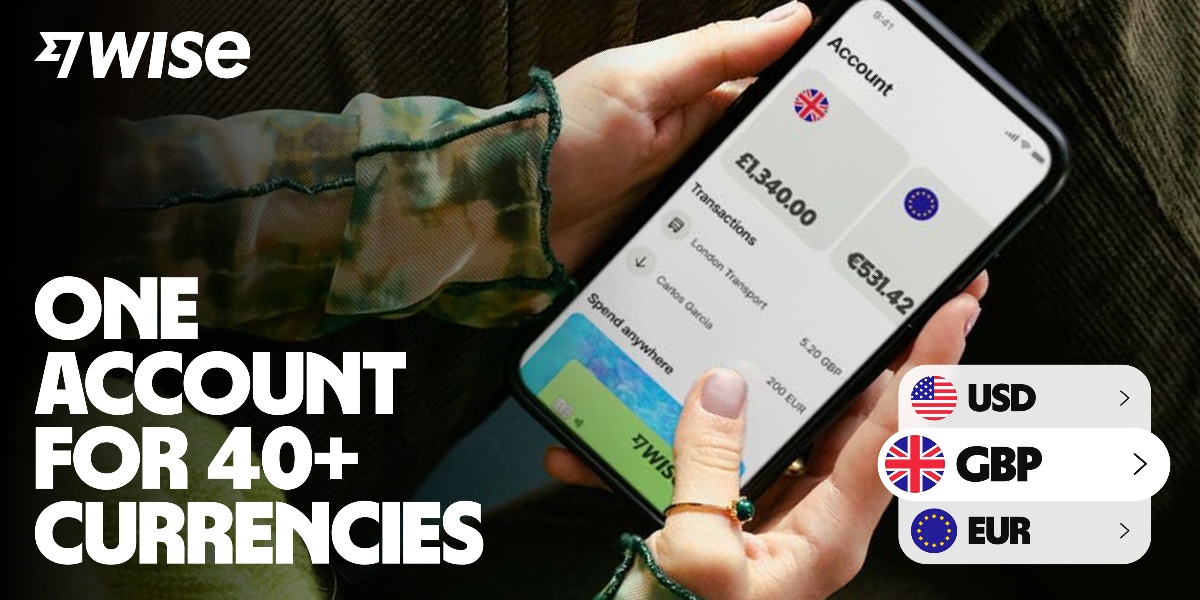

If you’re frequently travelling abroad or manage your money in multiple currencies, we’ll also show you an alternative from the money services provider Wise - the Wise account. It’s not a bank account but a travel-friendly, international account that offers some similar features, and your money is safeguarded.

Over 14.8 million people worldwide use Wise to send, spend and convert money in pounds, euros and 40+ more currencies – for low, transparent fees* and no-markup exchange rates close to what you can see on Google. Plus, you’ll get dedicated support and volume discounts when sending large amounts.

➡️ Learn more about the Wise account

In the UK, most everyday accounts can be opened online. Common types include:

Designed for everyday banking, these accounts let you make regular deposits and withdrawals, have your salary paid directly in and use a debit card for cash withdrawals and purchases. Many also offer extra services like arranged overdraft and travel insurance.

You can even open some current accounts for free.

As you might guess by the name, savings accounts are for setting money aside to earn interest rather than everyday spending. Typically, you get better interest rates on accounts that require a higher minimum deposit or that limit withdrawals.

These accounts let you hold money in more than one currency, which can come in handy for expats, cross-border professionals and frequent travelers.

Multi-currency accounts are typically made for speed and flexibility, with all-digital applications and quick approvals.

Not everyone qualifies for a regular bank account. If you’re unemployed, have bad credit or are just new to the country, you might only be eligible for a basic bank account.¹

These are accounts that the nine largest UK banks; Barclays UK, the Co-operative Bank, HSBC UK, Lloyds Banking Group, Nationwide Building Society, NatWest Group, Santander UK, TSB and Virgin Money, must offer by law to legal UK residents.² The accounts come only with basic services like depositing and withdrawing money, but also don’t charge monthly fees.

The exact process of opening an account online varies by bank, but here’s what the steps typically involve:

We’ve already gone over the types of bank accounts you can open online, so you should be able to choose one that best fits your situation. Do you want the account to pay everyday bills, to put money aside for a specific goal, to send funds abroad or something else? Your main purpose should guide your choice.

Once you’ve decided on the type of account, it’s time to compare the options out there. Some current accounts have no monthly fee, for example, while others do, but provide extra services you might find useful. For savings accounts, details like minimum balance requirements and rules about withdrawals are important to consider along with interest rates.

Now, you can start the application process. This usually means filling out basic details like your name, date of birth, and contact information on a webpage or app. You may also be required to agree to a credit check and asked about your address history, employment and income.¹ ³

You’ll also need to provide proof of identity and current address. We’ll go over the documents needed for this in more detail later. In many cases, you can upload scans or photos of your documents. Some banks may ask you to take a selfie with your phone or get on a short video call with a representative as a part of the verification process.⁴

Depending on the type of account, you may need to put in a starting deposit. Most UK current accounts let you open the account with a £0 balance and just transfer money in when you’re ready. But some savings accounts do require an initial deposit, even if it’s just £1, before they become active.⁵

Once you’ve submitted all your information, the bank will look over your application to decide whether or not to open the account. Usually, this process is pretty straightforward: The banks just want to confirm who you are, where you live, and in some cases, where your money comes from. For many bank accounts, this process takes just minutes, though it can take longer.

After your application’s approved, your bank will notify you and let you start using the account right away. You’ll be able to set up direct debits and transfers right from the app or website. Many banks will also give you a virtual debit card number immediately so you can make online purchases, and mail you the physical card by post.

Most adults living in the UK can open a basic bank account online. If you’re under 18, you may need a parent or guardian to apply with you or on your behalf to get the entire process done online.⁶

If you’re not living in the UK, however, you may have trouble opening a UK bank account. Many UK banks won’t let non-residents open or keep accounts, even if you hold British citizenship.⁷

And as we went over earlier, you need to be able to provide proof of identity and address digitally to open an account online. If the bank can’t verify these digitally, they may require you to visit a branch.

Can you open an account online as a student?

Yes, if you meet the requirements. Opening a student account online typically requires that you be a UK resident who is at least 17 years old and enrolled in a full-time education course.

For these accounts, you’ll need to prove your student status. Usually, this means providing a UCAS personal ID or an official university acceptance letter. Some accounts do come with additional requirements, like proof of having lived in the UK for 3 years or more.⁸

Otherwise, the application process is similar to opening a regular current account. Of course, you don’t have to get a student-specific account just because you’re a student. Regular current and savings accounts are options too, as long as you meet the requirements. The benefit of a student account is that it often comes with special perks like 0% interest overdraft or discounts from retailers.⁸

The documents you’ll need are pretty straightforward. You’ll basically just need to prove who you are and where you live. Depending on the type of account or your situation, though, the bank might ask for additional items. Typical documents include:

There’s no single best bank account, since what’s best for you depends on what matters most to you. If having a cash machine on every corner is the priority, a high street bank might work best, while if you want to save as much as possible, a competitive digital-only bank might offer you the best interest rate.

It’s also worth factoring in extras. Some banks offer switching bonuses or other perks, while others just focus on keeping costs low. Here are a few very different options to give you a sense of what’s out there.

For a full-service bank with the option of physical branches that still offer a good online experience, the high street names are a safe bet. Barclays, HSBC, Lloyds and NatWest all let you apply online and offer a broad range of products.

Some bigger banks have launched online brands that offer digital-only accounts. These brands are often set up to attract younger or digital-first customers but get FSCS protection through their parent bank. These include First Direct by HSBC, Marcus by Goldman Sachs, and Smile by The Co-operative Bank.⁹

Newer, app-first banks typically offer fast and easy app- or web-based experiences alongside lower fees. Some well-known brands include Starling and Zopa Bank, which offer current accounts,¹⁰ and Atom Bank, which focuses on savings.¹¹

Revolut is another major player: It has a UK banking license but, for now, is still operating as an electronic money institution while waiting for full approval. Other well-known fintech banks like N26 and Bunq aren’t open to new UK residents but may be an option for you if you live in the EU.

Here are the typical fees to consider before selecting a bank account:

If you’re looking for an international account instead that lets you manage your money in the UK and abroad, see if a Wise account might be a better fit for your needs. It's not a bank account but offers some similar features and your money is safeguarded.

| Here’s an overview of the main benefits of using Wise: |

|---|

|

**Investments in funds are never guaranteed and your capital can be at risk. In the UK, Interest and Stocks are provided by Wise Assets — this is the trading name of Wise Assets UK Ltd, a subsidiary of Wise. Wise Assets UK Ltd is authorised as an investment firm and regulated by the Financial Conduct Authority (FCA). Our FCA number is 839689. We do not give investment advice, and you may be subject to pay tax. If you're not sure, seek qualified advice. You can find more information about the funds on our website.

Sources used:

Sources last checked 29-Sep-2025

*Please see terms of use and product availability for your region or visit Wise fees and pricing for the most up to date pricing and fee information.

This publication is provided for general information purposes and does not constitute legal, tax or other professional advice from Wise Payments Limited or its subsidiaries and its affiliates, and it is not intended as a substitute for obtaining advice from a financial advisor or any other professional.

We make no representations, warranties or guarantees, whether expressed or implied, that the content in the publication is accurate, complete or up to date.

Read our roundup of the best savings accounts for non-UK residents, including options from Barclays, HSBC Expat, NatWest and Skipton International.

Check out our essential guide on how to open a bank account in Jersey as a British expat, including documents, fees, banks and much more.

Check out our essential guide on how to open a bank account in Monaco as a British expat, including documents, fees, banks and much more.

Check out our essential guide on how to open a bank account in Andorra as a British expat, including documents, fees, banks and much more.

Read our rundown of the best Nationwide USD account alternatives available in the UK, including HSBC, Lloyds, Wise, Barclays, Revolut and more.

Read our essential guide to the Revolut USD Account, including info on features, fees, rates, limits and how to apply.